How GCC Exchange Houses Redeploy Released Nostro Capital

GCC exchange houses that eliminate Nostro pre-funding free $15–25M overnight. Here is where that capital goes, and how it compounds.

Eliminating Nostro pre-funding across four to six active corridors frees $15–25 million in working capital for a mid-size GCC exchange house - capital that was generating zero return while sitting in pre-funded accounts waiting to be called on for settlement. That released capital does not sit idle for long. Exchange house CFOs in 2026 are moving it into three places: short-duration treasury yield instruments that generate $800K–$900K annually on $20 million deployed, FX spread repricing that converts the released financing cost into volume growth on competitive corridors, and new corridor expansion that adds revenue with near-zero capital requirement.

This article covers the mechanics of each deployment decision - with the calculations, the instrument categories, and the sequencing that experienced exchange house treasurers are applying in practice.

See how FLOW Send eliminates Nostro pre-funding →

How much capital does a GCC exchange house typically hold in Nostro accounts?

A mid-size GCC exchange house processing $40–60 million per month in outbound volume typically holds $15–25 million across four to six active Nostro accounts - one per corridor. A Nostro account (an account held at a foreign bank in the local currency of the destination corridor) must be pre-funded ahead of settlement. The pre-funding requirement reflects settlement lag: if a payment takes three to five days to clear locally after the SWIFT message is transmitted, the Nostro account must carry enough balance to cover outflows during that window without waiting for incoming replenishment.

The arithmetic is direct. A single corridor with $2.27 million in average daily volume ($50 million per month ÷ 22 working days) and a five-day settlement lag requires $11.35 million pre-funded to avoid a gap. Across four corridors of similar volume: $45 million in pre-funded capital, earning zero return.

That final point bears restating: zero. Nostro balances held at correspondent banks do not earn treasury yield. They are not invested. They are parked - a permanent float that the exchange house pays for implicitly through the opportunity cost of not deploying that capital elsewhere.

What are the three ways GCC exchange houses deploy released Nostro capital?

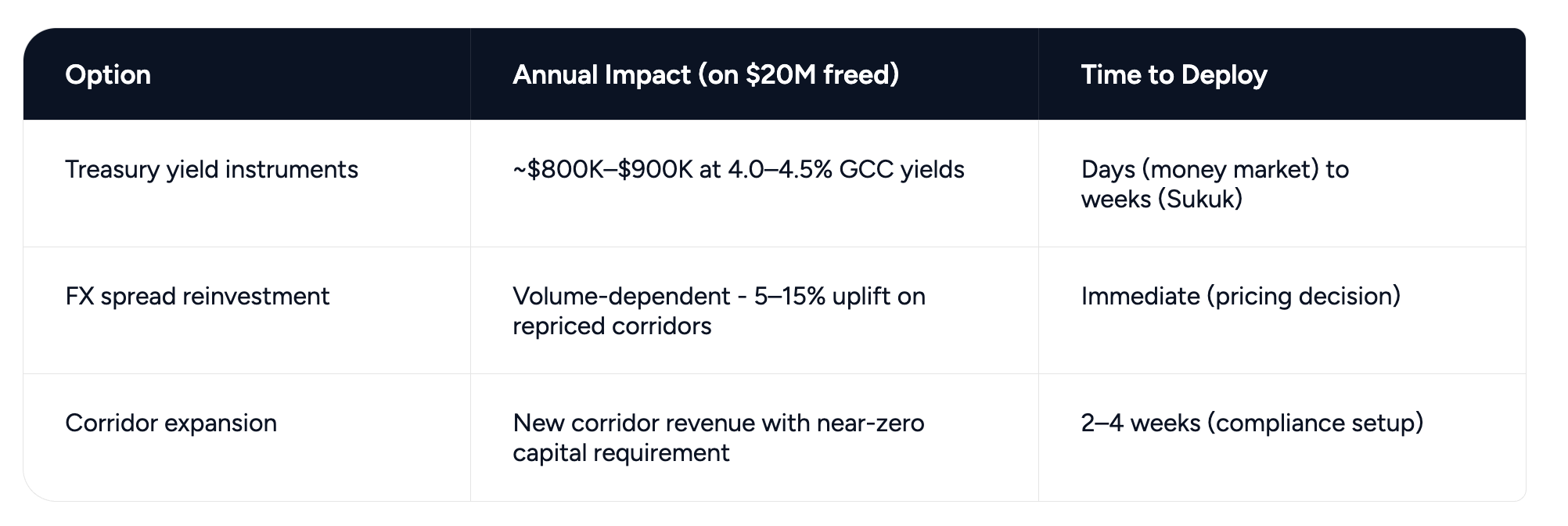

Released Nostro capital flows into three distinct applications, each with a different return profile and time-to-deploy horizon.

The sequencing matters. Treasury yield is the lowest-friction deployment - capital can be placed in short-duration instruments within days of the Nostro wind-down. FX pricing is an immediate commercial decision that costs nothing to implement once the Nostro financing cost is confirmed as eliminated. Corridor expansion requires compliance setup but no additional capital. Most exchange house CFOs run all three in parallel within the first quarter of the Nostro release.

How do GCC exchange houses earn yield on released Nostro capital?

Released Nostro capital earns yield by parking in short-duration GCC sovereign instruments rather than leaving it in pre-funded correspondent accounts. The instrument categories available to GCC-licensed exchange houses in mid-2026 cover a range of structures and Sharia-compliance profiles.

GCC government Sukuk. Bahrain sovereign Sukuk are yielding approximately 4.1%, Saudi T-bills approximately 4.2%, and UAE T-bills approximately 4.0%, based on mid-2026 issuance data from the respective central banks. For exchange houses operating under Sharia-compliant mandates, government Sukuk are the primary instrument category - they offer sovereign credit quality, secondary market liquidity, and compliance with Sharia principles on profit-sharing versus interest.

Institutional money market funds. Licensed GCC institutional money market funds offer daily liquidity and current yields in the 3.9–4.3% range - the closest equivalent to a cash position that earns a return. For exchange house treasurers who need to ensure capital is available on short notice (should volumes spike and require emergency pre-funding of a corridor), money market funds provide the liquidity profile that longer-duration instruments do not.

The calculation on $20 million deployed at 4.25% average: $850,000 in annual yield - a new revenue line that did not exist when that same capital was sitting at zero in Nostro accounts.

Duration matching is the constraint that shapes instrument selection. Released Nostro capital is freed working capital - it must remain accessible if settlement volumes on a corridor surge unexpectedly and temporary pre-funding is required. That argues for short duration: 30 to 90-day instruments rather than multi-year bonds. The $850,000 yield figure is achievable on a 90-day rolling position; it does not require locking into long-dated Sukuk, which would introduce mark-to-market risk and redemption constraints incompatible with a treasury management mandate.

How does released Nostro capital improve FX pricing competitiveness for GCC exchange houses?

Released Nostro capital improves FX pricing by eliminating an embedded cost from the spread that was previously required to make the Nostro position commercially viable. The mechanism is specific: exchange houses with Nostro pre-funding price their FX spread to include the implicit financing cost of holding the Nostro balance. That financing cost - at a GCC WACC of 7–8% on $15–25M - was embedded as margin, not disclosed as a fee. Eliminate the Nostro position, and the financing cost disappears from the spread calculation.

The illustration: if 30 basis points of a 120 basis point FX spread covers the implicit Nostro financing cost on a corridor, eliminating Nostro enables a sustainable 90 basis point spread that delivers the same net margin at higher volume. The exchange house is not cutting its margin - it is removing a cost from the stack that was always passed through to the customer.

Volume response on competitive corridors tends to be disproportionate. The India (INR), Pakistan (PKR), and Philippines (PHP) corridors are characterised by high frequency, repeat transactions, and price-sensitive customers who compare rates across three or four exchange houses before transacting. On those corridors, a 20–30 bps tightening in spread - made possible by eliminating the Nostro financing cost - produces volume growth that amplifies the pricing improvement into a compounding P&L effect.

How does freed Nostro capital enable GCC corridor expansion without additional capital commitment?

Under a SWIFT/Nostro model, opening a new corridor requires opening a new Nostro account and pre-funding it. For a corridor with $500K–$1M in average daily volume and a four-day settlement lag, that means $2–4M in new capital committed to zero-yield pre-funding before the first transaction clears. The capital decision and the commercial decision are inseparable.

Under a direct settlement rail, opening a new corridor requires compliance setup and counterparty onboarding - typically two to four weeks - but near-zero incremental capital. The licensed rail operator holds the pre-funded positions in the destination currency. The exchange house is not adding another zero-yield balance to its balance sheet.

The implication for an exchange house that has freed $20M from Nostro wind-down: that capital is not required to fund corridor expansion. Three to five new corridors can be opened simultaneously, on the basis of commercial viability alone, without the capital allocation decision that previously gated each one.

The corridors where this is most commercially relevant in 2026:

Pakistan. The UAE-Pakistan remittance corridor carries $7–8 billion in annual volume, with significant untapped share in B2B payments beyond remittances. An exchange house that previously avoided this corridor due to the Nostro pre-funding requirement for PKR can now enter on the basis of compliance setup alone.

Philippines. GCC-to-Philippines volume runs approximately $6 billion annually, driven by OFW remittances and a growing B2B trade layer. Philippine peso delivery has historically required a well-capitalised Nostro position due to local clearing structure - a direct rail removes that barrier.

Sub-Saharan Africa. The fastest-growing GCC trade corridor. Seven-to-ten day SWIFT settlement timelines on African routes make Nostro pre-funding requirements particularly capital-intensive per dollar of transaction volume. A direct rail that bypasses correspondent infrastructure changes the economics of African corridor entry entirely.

For a detailed analysis of how GCC exchange houses replacing MTO settlement are restructuring the corridor economics, that article covers the P&L model across the full switch.

The capital freed from Nostro is not a one-time event. It is a structural reconfiguration of the exchange house's balance sheet - one that compounds annually as yield accrues, spreads tighten, and new corridor revenue builds on a zero-capital foundation.

Frequently Asked Questions

What is Nostro capital and why does it get released?

Nostro capital is the pre-funded balance an exchange house holds in a foreign bank's account to cover settlement of outbound payments before incoming replenishment clears. It is released when the exchange house switches from SWIFT correspondent settlement to a direct rail - eliminating the settlement lag that required the float in the first place.

How much Nostro capital does a GCC exchange house typically hold?

A mid-size GCC exchange house processing $40–60 million per month across four to six corridors typically holds $15–25 million in Nostro accounts. The benchmark: two to five days of average daily volume per corridor held as pre-funding. At $2.27 million in average daily volume on a single corridor, a four-day lag requires $9 million pre-funded - earning zero return. (ARP Digital, The Cost of Dead Capital, 2026)

What is the safest way to invest released Nostro capital for a GCC exchange house?

Short-duration GCC sovereign instruments - government Sukuk and 90-day T-bills - offer the appropriate combination of credit quality, Sharia compliance, and liquidity for exchange house treasury deployment. At current GCC yields of approximately 4.0–4.5%, $20 million generates approximately $800K–$900K annually on a 90-day rolling position, with capital available on short notice if settlement volumes require emergency pre-funding.

How does eliminating Nostro pre-funding improve exchange house profitability?

Eliminating Nostro improves profitability through three simultaneous effects: treasury yield on the released capital ($800K–$900K annually on $20M), tighter FX spreads that drive volume growth on competitive corridors (by removing the embedded Nostro financing cost from the spread), and new corridor revenue with no additional capital commitment. These effects compound on each other from the first year.

Can GCC exchange houses open new corridors without Nostro accounts?

Yes. Under a direct settlement rail, new corridor entry requires compliance setup and counterparty onboarding - typically two to four weeks - but no Nostro pre-funding. The rail operator holds the pre-funded positions in the destination currency. An exchange house that has freed $15–25M from Nostro wind-down can open three to five new corridors simultaneously without committing that capital to new zero-yield accounts.