Why GCC Exchange Houses Are Replacing Their MTO: A Cost and Speed Analysis

How GCC exchange houses reduce international wire transfer costs: the MTO fee model, nostro capital drag, and the P&L case for switching to direct rails.

GCC exchange houses are moving away from MTO relationships because the combined cost of commission, FX spread markup, and correspondent banking fees is now quantifiable, and licensed alternatives settle same-day without pre-funded accounts. The data makes the case without equivocation: a mid-sized exchange house processing $1 million per day across five corridors holds $15–20 million in dead capital generating zero return, at an annual opportunity cost exceeding $1.4 million at current GCC weighted average cost of capital.

This article covers where that cost comes from, what the P&L looks like after switching, and how the transition actually runs. See how exchange houses work with ARP Digital →

What an MTO Relationship Actually Costs

The cost of an MTO relationship is not a single fee — it is three extraction layers applied simultaneously, on every transaction, on every corridor. Most exchange house P&Ls capture the first layer. The second and third are structurally obscured.

Layer 1 - MTO commission. MTOs charge a per-transaction or percentage fee for access to their settlement network. For mid-volume exchange houses without significant negotiating leverage, this runs 0.5%–1.5% of principal. On a $20,000 business transfer, that is $100–$300 per transaction before any other cost is applied.

Layer 2 - FX spread markup. The MTO sets the conversion rate. The margin between the mid-market rate and the rate offered to the exchange house is the MTO's primary profit mechanism — and the least visible cost in the stack. On a $20,000 payment, a 1.5% FX spread is $300 that never appears as a labelled line item. The exchange house sees a blended rate; it rarely sees the markup.

Layer 3 - SWIFT correspondent fees. When the MTO routes through SWIFT correspondents, which most do for major volume corridors, the full institutional cost stack applies:

- Initiation fee: $25–$50 fixed per transaction

- Correspondent lifting fees: $5–$30 per intermediary hop

- FX spread markup at each hop: 0.5%–2.0% of principal

The World Bank's Q3 2025 data puts the global average cost of sending $200 at 6.36%. The MENA average sits at 6.25%. Sub-Saharan Africa, one of the GCC's fastest-growing disbursement corridors, runs at 8.78%. These are not marginal costs. They are the structural baseline the exchange house is working from before a single basis point of margin is earned.

The hidden operational cost sits alongside the financial one. Up to 50% of delayed or failed SWIFT payments result from simple data errors: unstructured beneficiary addresses, incorrect account formats, missing reference codes. Each requires manual investigation that consumes treasury headcount, headcount that is not processing volume.

The Nostro Burden - Capital You're Holding for Free

An exchange house does not manage one corridor. It manages separate, non-fungible liquidity pools for each. Excess INR cannot cover a PKR shortfall without additional FX conversions. Excess AED cannot fund a delayed PHP payout without a round-trip through a correspondent. Each pool must be sized independently, held continuously, and replenished as transactions clear.

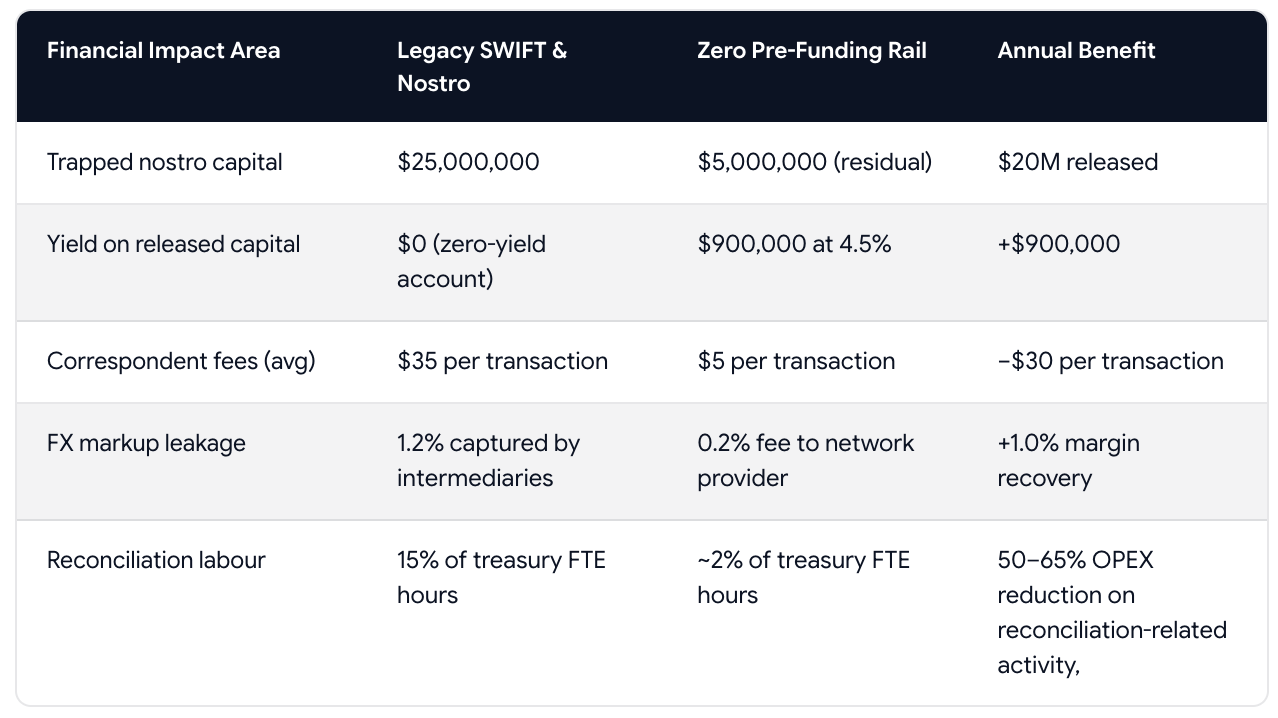

The number this produces is not intuitive until it is calculated. A mid-sized exchange house processing $1 million per day across five corridors - GCC-to-India ($50–55 billion annually), Saudi-to-Pakistan ($8–9 billion), UAE-to-Pakistan ($7–8 billion), and comparable tier-two corridors - with a 3–4 day SWIFT settlement lag must hold $15–20 million in pre-funded nostro capital at any given moment. That capital earns zero return.

The cost of holding dead capital was tolerable when interest rates were near zero. At a GCC WACC of 7–8% today, the annual drag on $15–20 million in trapped capital exceeds $1.4 million, before a single SWIFT fee or FX spread is applied.

The flip side is equally concrete. Releasing $20 million from nostro accounts and deploying at current GCC treasury yields of 4.0%–4.5% generates approximately $900,000 in annual passive income, independent of transaction volume. The yield generated by not holding dead capital frequently funds the entire integration project.

The Al Ansari Financial Services FY2025 results illustrate the scale at which this problem compounds: the group reported AED 3.84 billion ($1.04 billion) in "Cash in hand, Due from banks" - a 32.7% year-on-year increase. For a listed exchange house, that balance is visible to investors. For a private exchange house, it is quietly eroding equity returns every quarter.

The full corridor-by-corridor cost model and CFO decision framework is available in The Cost of Dead Capital report. Download The Cost of Dead Capital report →

What the P&L Looks Like After Switching

A direct settlement rail does not improve the P&L marginally, it transforms the cost structure on both sides of the ledger simultaneously.

The margin recovery arithmetic is direct. If total SWIFT deductions average 1.5% of principal and the direct settlement rail charges 0.5%, that 100 basis point differential drops to EBITDA on every transaction processed. For an exchange house moving $1 million per day, that differential compounds to approximately $3.65 million per year, before the capital yield improvement is counted.

Settlement speed is the second dimension of the improvement. T+0 atomic settlement on stablecoin rails versus T+3 to T+15 on SWIFT. On African corridors, now among the GCC's fastest-growing disbursement markets, SWIFT settlement currently runs 7–15 days due to capital controls and local clearing constraints. For an exchange house running a Ghana or Kenya corridor, T+0 is not a feature comparison. It is the difference between a viable commercial offering and one that loses clients to competitors on settlement reliability alone.

FLOW Send operates on this model - two domestic legs, no correspondent chain, no pre-funded nostro account required. Download the full cost analysis →

How the Switch Actually Works

The transition from correspondent banking to direct settlement infrastructure is a treasury transformation programme. Exchange houses that treat it as a technology procurement stall. Those that treat it as a phased treasury initiative, with defined ROI gates at each phase, complete it within 6–12 months

Phase 1 - Audit. Map current nostro balances per corridor. Calculate the exact trapped capital figure and the FX margin surrendered to correspondents on each route. This produces the ROI case the board needs to approve the migration budget, and it almost always produces a larger number than the CFO expected.

Phase 2 - Pilot corridor. Start with a high-friction, low-efficiency corridor, typically Sub-Saharan Africa or a tier-two South Asian market. Route 10% of daily volume through the new rail while 90% stays on legacy infrastructure. Verify settlement finality, fee elimination, and API integration with the core banking system before committing broader volume. The pilot corridor produces auditable performance data against which the legacy cost is directly comparable.

Phase 3 - Wind-down and capital release. Migrate bulk volume. Instruct the legacy correspondent to wind down the nostro balance. Released capital is redeployed to the treasury allocation. The implementation window - including KYB onboarding, ISO 20022 upgrades where applicable, and staff retraining - realistically runs 6–12 months end to end.

Frequently Asked Questions

Why are GCC exchange houses moving away from MTOs?

MTO relationships extract commission, FX spread markup, and correspondent fees simultaneously, costs that compound across corridors and volume. Direct settlement infrastructure with no pre-funding requirement eliminates the intermediary layer and recovers margin at every transaction.

How much capital does an exchange house need to hold in nostro accounts?

A mid-sized GCC exchange house processing $1 million per day across five corridors must hold $15–20 million in pre-funded nostro capital at any given moment, earning zero return, at an annual opportunity cost exceeding $1.4 million at current GCC WACC.

What does stablecoin settlement mean for an exchange house's compliance obligations?

A licensed stablecoin settlement provider operates under the same AML, KYC, and transaction monitoring requirements as a traditional financial institution. The exchange house retains due diligence responsibility over its choice of provider, it does not absorb incremental compliance risk.

How long does it take to transition away from correspondent banking?

A phased transition - audit, pilot corridor, wind-down - realistically takes 6–12 months including core banking upgrades and staff retraining. Institutions that treat it as a treasury programme rather than a technology project complete it faster.