The True Cost of SWIFT for GCC Businesses: Fees, Delays and Hidden Charges

A $10,000 SWIFT transfer from the GCC can cost $189 in hidden deductions before reaching your supplier. Here's every layer, calculated.

A SWIFT transfer from a GCC business account carries four cost layers: the sending bank's initiation fee ($25–$50), correspondent lifting fees deducted by each intermediate bank ($10–$30 per hop across 2–4 banks), an FX spread of 0.5–2.0% of principal applied at each currency conversion, and a settlement window of T+1 to T+5 on standard corridors that carries its own treasury cost. The fee shown on the bank statement is only the first layer, and typically the smallest.

GCC businesses are expanding across corridors - China, India, Pakistan, Sub-Saharan Africa - where every additional hop in the correspondent chain adds cost and time. This article covers all four cost layers, what the shortfall looks like on the beneficiary's side, and what a multi-day settlement window actually costs a treasury.

See how FLOW Send removes the correspondent chain →

The Fee the Bank Tells You About

The sending bank charges a fixed initiation fee for processing the SWIFT instruction: typically $25–$50 per transaction, regardless of the amount being transferred. This fee appears on the statement. For most GCC businesses, it is the only cost they see.

What the initiation fee covers: the cost of generating and transmitting the SWIFT message to the first correspondent in the chain.

What it does not cover: any fee charged by correspondent banks further along the route, any FX conversion applied between the sending bank and the beneficiary's institution, or any delay caused by data validation failures at intermediate banks.

One point of terminology worth stating clearly: the initiation fee is the sending bank's charge for using the SWIFT network, not a charge from SWIFT itself. SWIFT, as a cooperative, charges its member banks for network access. Those costs are passed through as the initiation fee on the customer's statement. The distinction matters because it clarifies where subsequent costs originate: from the correspondent banks in the chain, not from SWIFT as an entity.

On a $5,000 B2B transfer, a $35 initiation fee represents 0.7% of principal, before the transfer has cleared a single correspondent bank.

The Correspondent Chain - Where Fees Multiply

Most SWIFT transfers between GCC businesses and international counterparties pass through 2–4 correspondent banks before reaching the destination institution. Each correspondent in the chain validates the transaction against its own AML and compliance requirements, deducts a lifting fee from the principal ($10–$30 per hop), and passes the remainder to the next bank.

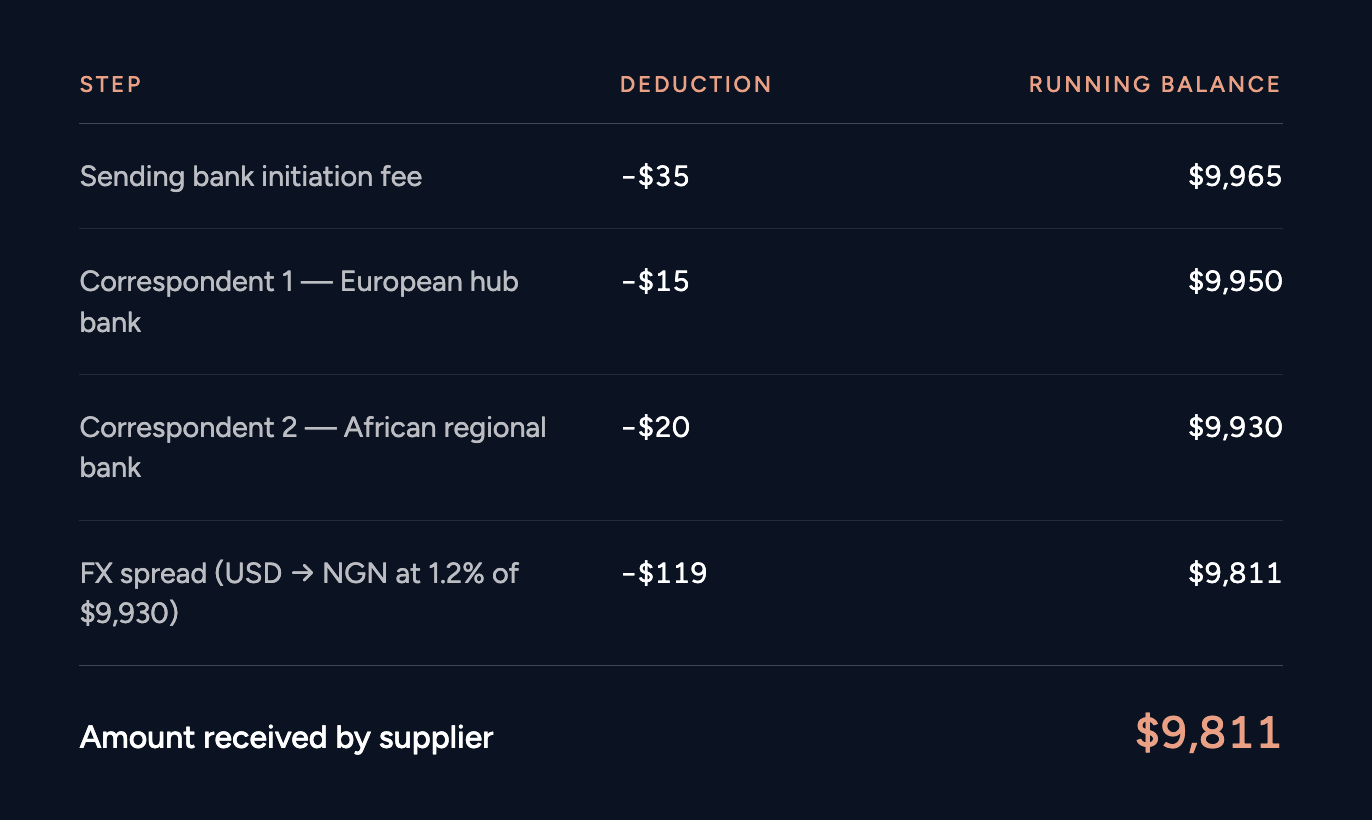

The arithmetic on a real transaction (as an example):

$10,000 sent from a UAE business to a supplier in Nigeria

The supplier received $189 less than invoiced. The UAE business sees $35 on their bank statement.

Under the current SWIFT architecture, the sending business receives no automated notification that the beneficiary received less than the instructed amount. The first signal is typically a query from the supplier, sometimes days after the transfer was sent.

The shortfall is further compounded by data quality. Up to 50% of delayed or failed SWIFT payments are caused by data errors: an unstructured beneficiary address, an incorrect IBAN format, a mismatched account name. Each triggers a manual investigation cycle that can add days to resolution and, in some cases, result in the funds being returned minus processing fees already deducted. (ARP Digital, The Cost of Dead Capital, 2026)

For exchange houses managing this cost stack across five or more corridors simultaneously - at daily volumes that make each basis point material - the aggregate drag runs into millions annually. The mechanics of that calculation are covered in our analysis of GCC exchange house settlement costs →

The FX Spread - The Cost That Never Appears on the Invoice

When a SWIFT transfer involves a currency conversion - AED to INR, AED to USD, USD to PKR - each bank in the chain that handles the conversion applies its own spread between the mid-market rate and the rate it offers. This spread is not disclosed as a line item on any document the business receives. It appears as a smaller-than-expected amount arriving in the destination currency.

The range: 0.5–2.0% of principal per conversion.

On a multi-conversion corridor - AED through USD to PKR - two conversions are applied. At 1.0% per conversion, the FX cost alone is approximately 2.0% of the principal before any lifting fee is counted. On a $50,000 supplier payment, that is $1,000 that does not appear on any invoice or statement the business receives.

The World Bank Remittance Prices Worldwide report (Q3 2025) measures the total cost - fees and FX margin combined -of sending $200 internationally. The global average is 6.36%. MENA sits at 6.25%. Sub-Saharan Africa, one of the GCC's fastest-growing trade corridors, reaches 8.78%.

The G20 committed in 2020 to reducing the global average cost of international transfers to 3% by 2030. As of Q3 2025, the global average remains at 6.36% - more than double the target. The MENA average has not moved materially toward that threshold. (World Bank, Q3 2025)

The FX spread is, on most GCC international transfers, the largest single cost component, and the one least likely to appear on any document the business receives.

What the Settlement Delay Actually Costs

A SWIFT transfer is not settled when it leaves the sender's bank. It settles when it clears local infrastructure at the destination, a process that takes T+1 to T+5 business days on standard corridors, and longer on more constrained routes.

SWIFT's own data shows that 90% of payments reach the destination bank within one hour of transmission. Only 43% reach the end customer's actual account in that same window. The destination bank is not the beneficiary. It is the last correspondent in the chain. The payment then enters local clearing - RTGS, ACH, or manual processing depending on the destination market - before it reaches the supplier's account. In markets with less developed clearing infrastructure, this final leg can take days.

We have seen finance teams treat this distinction as a technicality until it becomes a supplier relationship problem, when a supplier in Nairobi or Karachi expects payment within two days of receiving confirmation and the funds do not arrive for eight.

The cost of the delay is not only relational. For a GCC business making a $500,000 supplier payment that sits in the SWIFT pipeline for five business days, seven calendar days including the weekend, the opportunity cost at a GCC weighted average cost of capital of 7–8% is approximately $671–$767 for that window alone. Across a business making 20 comparable transfers per month, the annual drag from working capital committed and unavailable during settlement windows is material, and entirely absent from any invoice the finance team receives.

For GCC businesses trading with Sub-Saharan Africa, a corridor growing at pace with intra-African trade expansion, SWIFT settlement can extend to 7–10 business days in the most constrained cases, due to local capital controls and clearing infrastructure limitations.

Frequently Asked Questions

What does a SWIFT transfer actually cost a GCC business?

A SWIFT transfer from a GCC business carries four cost layers: the sending bank's initiation fee ($25–$50), correspondent lifting fees ($10–$30 per hop across 2–4 banks), an FX spread of 0.5–2.0% per conversion, and a settlement window of T+1 to T+5 on standard corridors. The total regularly exceeds 3–5% of principal on cross-currency corridors.

Why does a supplier receive less than the amount sent via SWIFT?

Each correspondent bank in the SWIFT chain deducts a lifting fee from the principal before passing the remainder to the next bank. By the time the transfer reaches the beneficiary institution, multiple deductions have reduced the original amount. The sender typically sees only the initiation fee on their own statement, not the intermediary deductions.

How long does a SWIFT transfer take to settle in the GCC?

SWIFT's own data shows 90% of payments reach the destination bank within an hour, but only 43% reach the end customer's account in that same window. The destination bank is the last correspondent, not the beneficiary. Local clearing adds T+1 to T+5 business days on standard corridors; African corridors can extend to 7–10 days. (ARP Digital, The Cost of Dead Capital, 2026)

What is the GCC average cost of an international transfer?

The World Bank Remittance Prices Worldwide report (Q3 2025) places the MENA average cost of sending $200 internationally at 6.25%, nearly double the G20 target of 3% by 2030. This includes both bank fees and FX spread margins applied along the transfer route.

What is an alternative to SWIFT for GCC businesses making cross-border transfers?

Licensed settlement infrastructure using local rails and stablecoin middleware eliminates correspondent banks from the route entirely. Two domestic legs - one in the sending currency, one in the receiving currency - settle the transfer without the correspondent fee stack or multi-day clearing window. Settlement completes at T+0 to T+1 depending on the corridor.