Same-Day Supplier Payments from GCC to India: The Complete Business Guide for 2026

GCC importers paying India suppliers via SWIFT lose up to $120 per transfer and 2–5 days to the correspondent chain. There's a licensed alternative.

GCC businesses can pay India suppliers without SWIFT by using regulated operators with direct INR settlement rails, no correspondent bank chain, no T+2 delay, and no per-hop fee deducted in transit. Settlement through this route completes within the same business day. SWIFT became the default because it was, for a long time, the only infrastructure available. Direct rail alternatives now exist, operated by licensed entities and regulated at the same level as the banks they replace. This guide covers what SWIFT actually costs on the GCC-India corridor, how direct settlement works, and what to look for in a provider.

See how much your transfers actually cost

Why SWIFT Creates Problems for GCC-India Supplier Payments

Every GCC importer we speak with has a version of the same story: the payment left on Monday, the supplier chased on Thursday, and nobody, not the sender, not the bank, could say where it was.

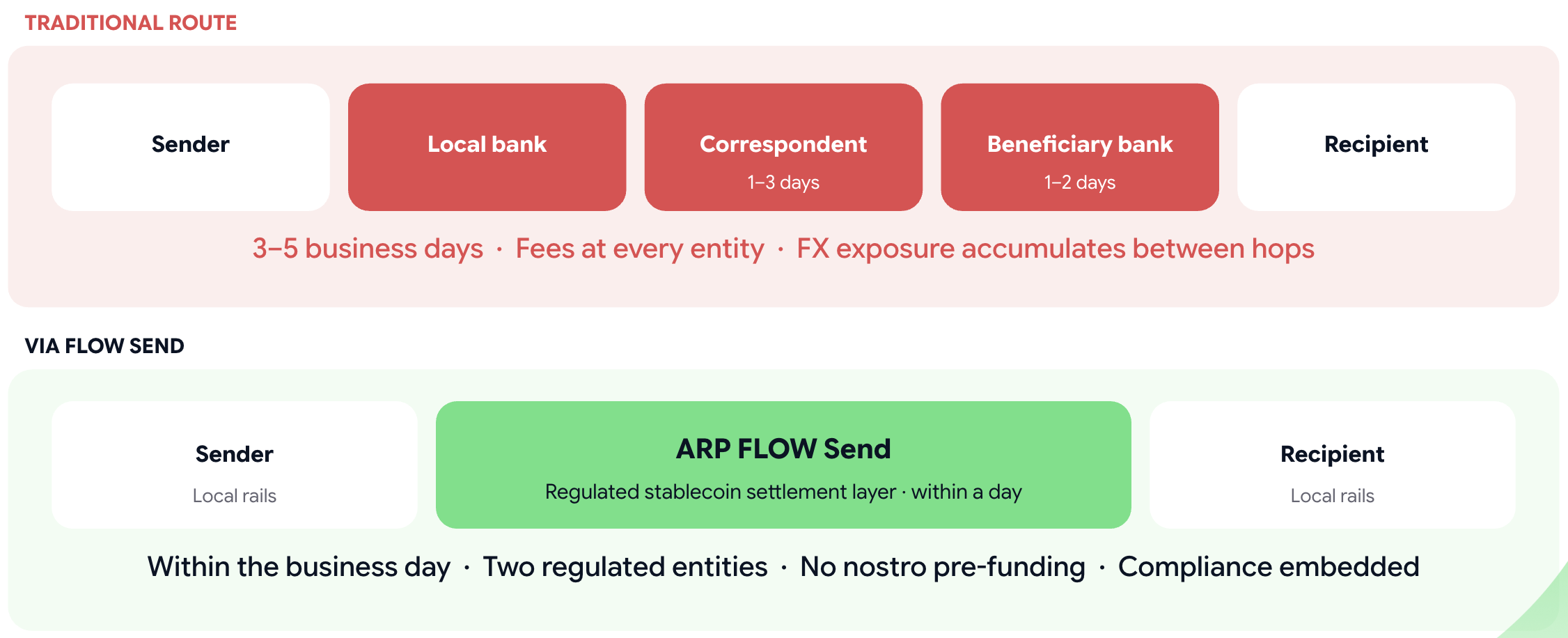

The correspondent chain is why. A SWIFT wire from a UAE or Bahrain bank to an Indian supplier does not move directly between those two banks. It routes through 2–3 correspondent banks: the UAE bank sends an instruction to its US correspondent, which forwards to an India correspondent, which finally credits the recipient's bank. Each institution confirms before the next acts. T+1 minimum per hop, before any compliance screening or time zone gap is accounted for. Total transit: T+2 to T+5 business days on a corridor that handles the largest remittance volumes in the GCC.

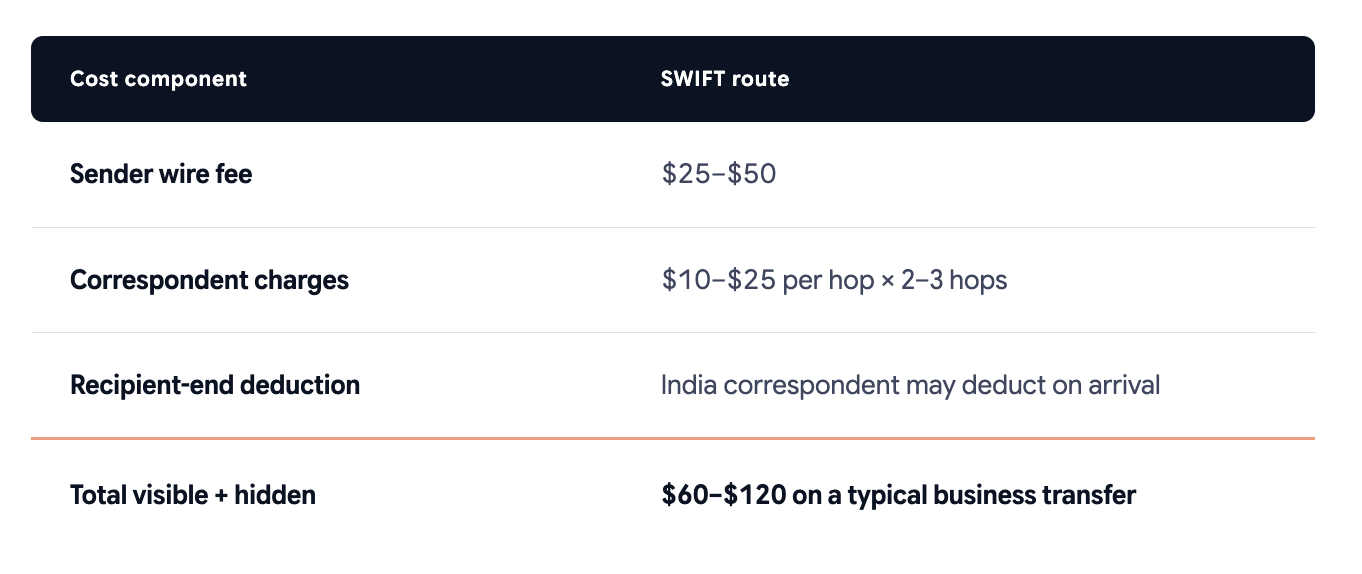

Each correspondent node also deducts a fee. The sending bank's wire charge runs $25–$50. Each intermediary deducts $10–$25 for processing. None of this is disclosed at the time of sending, the deductions arrive as a shortfall when the supplier reports receiving less than expected.

The FX spread adds a third layer. Banks set their own AED-to-INR rate, typically 1.5%–3.5% above mid-market. On a $20,000 supplier payment, that is $300–$700 in margin that does not appear as a fee, is not negotiable, and is often only visible in retrospect.

ARP Digital's 2026 survey of 200+ Bahrain-based SMEs found that 47% cite settlement delays as their primary payment problem (ARP Digital, SME Payments Survey, Bahrain, 2026). For businesses paying Indian suppliers on a monthly or weekly cycle, that statistic is not abstract, it is strained supplier relationships and disrupted production schedules.

A licensed alternative now exists that bypasses the correspondent chain entirely.

How Same-Day GCC-to-India Payments Actually Work

The speed difference between SWIFT and direct rail is structural. The reader who understands why will trust the route with a $30,000 transfer. The one who does not will default back to their bank.

The SWIFT route: Your bank issues a SWIFT instruction to its US correspondent. The US correspondent verifies and routes to an India correspondent. The India correspondent credits the recipient's bank. Each step waits for the prior step to complete. The chain is only as fast as its slowest node,and when a node holds the payment for compliance review, no one notifies the sender.

The direct rail route: ARP Digital’s FLOW platform accepts the payment in BHD and other GCC currencies and converts it to a regulated stablecoin, which settles across the GCC-India corridor within the business day. On the India side, a regulated counterparty converts the stablecoin to INR and credits the recipient's bank account via local rails. No correspondent bank. Two regulated entities. One settlement event.

What Does It Cost to Pay an India Supplier from the GCC?

Two cost components determine the real price of a GCC-India supplier payment: the transaction fee and the FX rate. SWIFT structures both to make the total difficult to calculate before the payment leaves.

Transaction fees, SWIFT vs. direct rail:

FX rate,SWIFT vs. direct rail:

Banks apply 1.5%–3.5% above mid-market for AED-to-INR. On a $20,000 payment, that is $300–$700 embedded in the exchange rate before the transfer is initiated.

A worked example: a $15,000 payment to an India textiles supplier via SWIFT. Wire fee: $40. Two correspondent deductions: $20 each. FX markup at 2.5%: $375. Total cost before the supplier receives anything: approximately $455, across three separate charges that never appear together on a single statement.

These costs do not appear as a single line on your bank statement. The wire fee is one charge. The FX margin is embedded in the exchange rate. Correspondent deductions appear as a shortfall when your supplier reports receiving less than expected.

Regulatory Requirements, What You Need to Send Money to India

GCC business owners often assume that using a licensed fintech means stepping outside their bank's regulatory perimeter. The position is straightforward: licensed operators are a legal, supervised route for cross-border business payments, subject to the same AML and KYC obligations as any bank.

On the sending side (GCC). The payment must originate from a licensed operator. The sender provides standard KYC documentation and a payment purpose, the same information a bank requests before processing a wire.

On the receiving side (India). India's Foreign Exchange Management Act (FEMA) governs all inbound international transfers. The recipient's bank may ask them to declare the payment purpose for transfers above certain thresholds, trade payment, advance against invoice, services rendered. This is routine Indian banking procedure, identical to what happens when a SWIFT wire arrives from abroad. Attaching an invoice reference to the transfer reduces the likelihood of the recipient bank requesting additional documentation.

Documentation checklist for the sender:

- Beneficiary full legal name (exactly as it appears on their bank account)

- Indian bank account number

- IFSC code,the 11-character routing code identifying the specific branch

- Payment amount and currency

- Payment purpose or invoice reference

The compliance requirements for a licensed fintech route are the same as SWIFT. The settlement path is different. The regulatory standard is not.

What to Look for in a Same-Day GCC-to-India Payment Provider

Once a GCC business decides to move away from SWIFT on the India corridor, four criteria separate providers that can deliver same-day settlement from those that cannot.

A regulated licence in the sending jurisdiction. A money services business registration is not equivalent to a Central Bank licence. A licensed operator has access to local settlement rails and is subject to ongoing regulatory oversight.

A direct settlement rail, no correspondent bank. Ask explicitly: does this payment pass through a correspondent bank? If yes, same-day settlement on the India corridor is operationally impossible. A direct rail means the provider maintains a pre-funded position in India and routes payments through RTGS directly to the recipient's bank. The answer to this question determines whether the speed claim is real.

A confirmed exchange rate before authorisation. The rate should appear on the confirmation screen, before you approve the payment, not after. If the exchange rate is only visible on the receipt, the spread was set after the funds were committed. A transparent rate disclosed at initiation is the minimum standard for a provider worth using.

A published cut-off time for same-day processing. Same-day means same-day if the payment is submitted before a specific time. Any provider offering this service states the cut-off clearly. Ask for it before onboarding. A provider that cannot give a specific time cannot guarantee the outcome.

A licensed operator with a direct INR rail, a pre-confirmation rate, and a disclosed cut-off can settle GCC-to-India supplier payments within the same business day. For more on how GCC SMEs are approaching cross-border payment infrastructure, the SME importer services page covers the full picture.

Frequently Asked Questions

How do I send money from Bahrain to India without SWIFT?

Use a licensed payment operator with a direct INR settlement rail, no SWIFT, no correspondent bank chain. The payment converts to a regulated stablecoin, crosses the corridor within the business day, and settles in INR via local rails on the India side. The process requires standard KYC, the beneficiary's IFSC code, and a payment purpose reference. Settlement typically completes the same business day.

How long does a GCC-to-India supplier payment take?

Through a standard SWIFT route, GCC-to-India payments typically settle in T+2 to T+5 business days, depending on the correspondent chain. Through a direct rail with no correspondent bank, BHD-to-INR payments can settle on the same business day, provided the payment is submitted before the operator's stated cut-off time.

What are the fees for sending AED to INR for business payments?

SWIFT transfers to India carry layered costs: the sender's wire fee ($25–$50), correspondent bank charges ($10–$25 per hop across 2–3 hops), and an FX margin of 1.5%–3.5% embedded in the exchange rate. A licensed operator with a direct rail charges a flat fee and shows the confirmed exchange rate before payment authorisation.

Is it legal to use a fintech to pay India suppliers from the GCC?

Yes. Payments through a licensed operator comply with GCC cross-border payment regulations. On the India side, incoming trade payments are governed by FEMA. The receiving business's bank may request a purpose declaration, the same documentation required for a SWIFT transfer. No additional regulatory steps apply.

What details do I need to pay an India supplier from the GCC?

You need the beneficiary's full legal name as it appears on their bank account, Indian bank account number, IFSC code (the 11-character branch routing identifier), payment amount, and a payment purpose reference or invoice number. These are the same details required for any cross-border business payment to India.

ARP Digital's 2026 survey found that 67% of GCC SMEs were ready to switch to a regulated payment provider that delivered faster settlement, FLOW operates under CBB Category 3 licensing, at the same regulatory standard as the banks it replaces

See How FLOW Handles the India Corridor →