GCC SME Cross-Border Payments: The 2026 State of Play

Primary research across 200+ GCC and MENA SMEs, February 2026: 47% cite settlement delays as their primary pain; 16% cannot quantify what they pay per transfer; 67% would switch to a regulated non-bank alternative.

The Scale of the Problem

GCC SMEs represent up to 96% of all registered companies in the MENA region and account for roughly half of total regional employment. The global cross-border payments market, valued at approximately USD 212.55 billion in 2024, is projected to reach USD 320.73 billion by 2030 at a CAGR of 7.1% (Grand View Research). The B2B segment commands 72.6% of all transaction volumes. GCC businesses are executing this trade at volume, but on infrastructure built for institutions, not for the businesses that now drive the most significant share of regional commercial growth.

The data from ARP Digital's 2026 GCC SME survey makes the operational reality concrete. Only 16% of respondents achieve same-day settlement on cross-border payments. 23% pay over 1% per transfer. 16% cannot quantify what they pay at all. One electronics importer in the survey reported an average of 20 days to clear a payment to a Chinese supplier. A manufacturing firm described a European payment held for three months by a compliance review, with no proactive notification from the bank that the payment had stalled.

These are not anomalies. They are the upper end of a spectrum of failures that are endemic to the multi-hop correspondent banking architecture GCC SMEs navigate every month.

Download the full report, including raw survey data, corridor breakdowns, and buyer segment analysis: The Infrastructure Gap: GCC SME Cross-Border Payments 2026

Why Is GCC Trade Shifting East and Why Does It Matter for Payments?

GCC trade is reorienting from West to East at a scale that has directly outpaced the financial infrastructure designed to support it. Trade between the Gulf and Asia reached USD 516 billion in 2024, nearly double the USD 256 billion registered in Gulf-West trade (Global Trade Review, 2026). Bilateral flows between the Gulf and China alone rose to USD 257 billion, surpassing the combined value of GCC trade with the United States, the United Kingdom, and the Eurozone for the first time in modern economic history.

This reorientation matters for payments because the traditional correspondent banking infrastructure serving GCC SMEs was built around established Western corridors. It was not built for high-frequency, mid-size B2B transactions flowing to Shenzhen electronics suppliers or Guangzhou manufacturers. The result is a widening mismatch: trade volumes are expanding on corridors where banking infrastructure is thinnest and correspondent relationships are fewest.

Sources: Global Trade Review (GTR), 2026; Grand View Research Cross-Border Payments Market Report

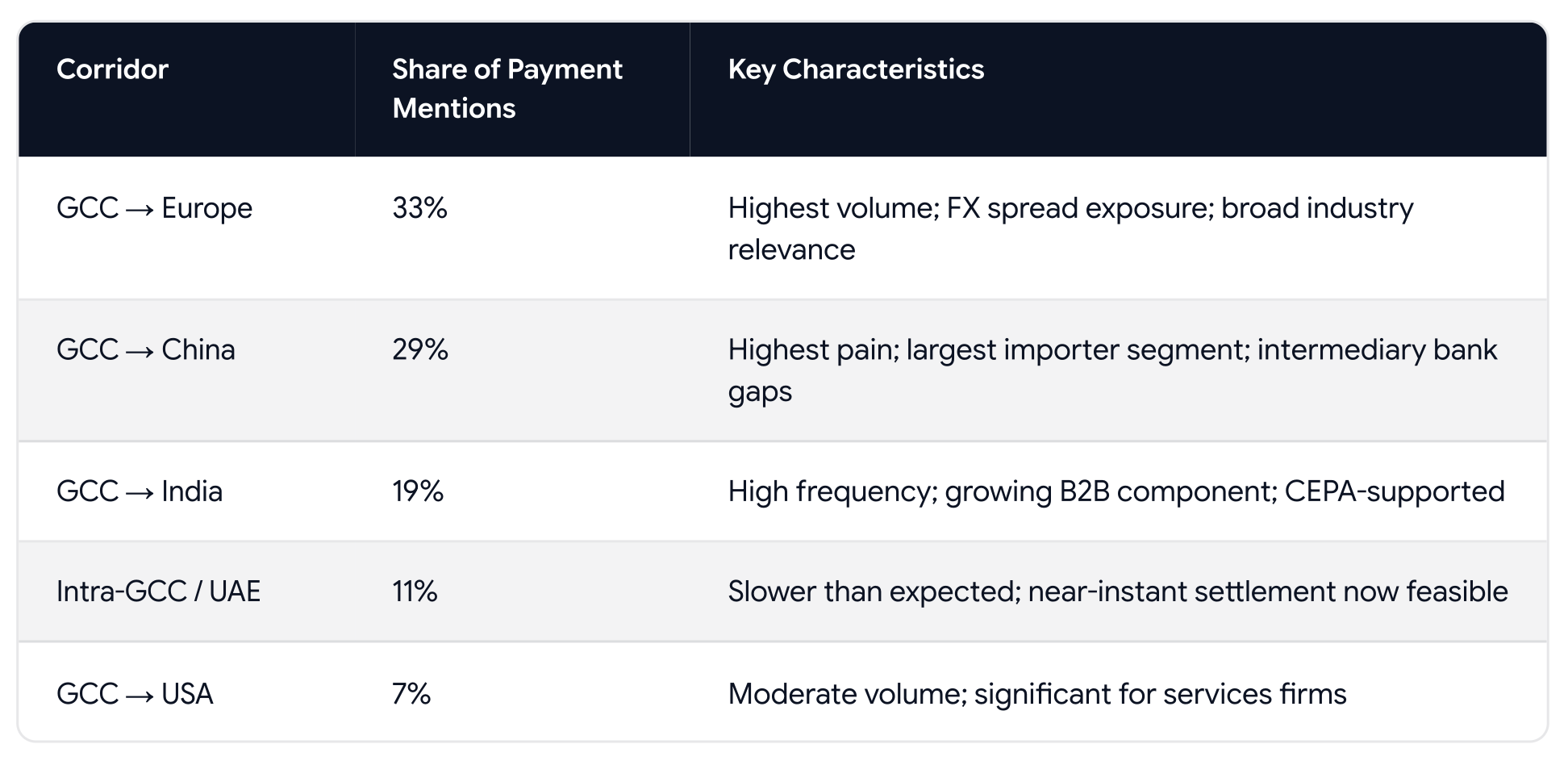

GCC SMEs sit directly at the intersection of this trade expansion. In ARP Digital's 2026 survey, 29% of all payment mentions were China-bound and 33% were Europe-bound. These two corridors alone account for 62% of payment volume in the surveyed sample, yet they are precisely the corridors where the correspondent banking system performs most poorly.

What Is Keeping GCC SMEs Locked Into Underperforming Banking Infrastructure?

Three structural forces keep GCC SMEs dependent on banking infrastructure that consistently fails them: correspondent bank de-risking, the hidden architecture of FX markup costs, and the absence of a credible regulated alternative they have been offered.

Correspondent Bank De-Risking

Cross-border payments rely on correspondent banking relationships (CBRs) - the links between domestic institutions and foreign intermediaries that allow a bank to clear transactions in jurisdictions where it has no physical presence. Over the past decade, global tier-one banks have systematically withdrawn these relationships in emerging and frontier markets, including MENA, in response to escalating AML/CFT compliance mandates.

The logic is asymmetric: the cost of due diligence on high-volume, low-value SME transactions routinely exceeds the fee income generated. Faced with the risk of large regulatory fines, major clearing banks have moved to wholesale risk avoidance rather than targeted risk management, terminating entire regions, corridors, and client classes. The FATF itself has noted that this de-risking behaviour, by pushing legitimate flows into less transparent channels, runs counter to the risk-based approach it was designed to promote.

The second-order effects for GCC SMEs are direct. Domestic banks stripped of their primary correspondent links are forced into replacement relationships with smaller intermediaries. A payment that once required a single correspondent hop may now pass through three or four intermediary banks before reaching a supplier in China or Europe. Each additional hop adds cost, settlement time, and opacity to a transaction that was already too expensive and too slow.

Information Asymmetry: Zero Tracking

Once a payment leaves a domestic account, GCC SMEs typically receive no real-time visibility into routing path, intermediary banks involved, or final deduction amounts. The legacy SWIFT architecture does not provide a unified, end-user-accessible tracking standard. Critical payment data is frequently lost, truncated, or stripped as instructions pass between proprietary systems operating in different jurisdictions and time zones.

In ARP Digital's 2026 survey, 7% of respondents identified lack of transparency as a primary pain point — but this figure significantly understates the problem. The qualitative interviews reveal that the majority of respondents have simply normalised opacity: they do not know what they don't know. The manufacturing firm that waited three months for a European payment to clear did not know it had stalled until a supplier relationship had already been damaged.

The Absence of Alternatives

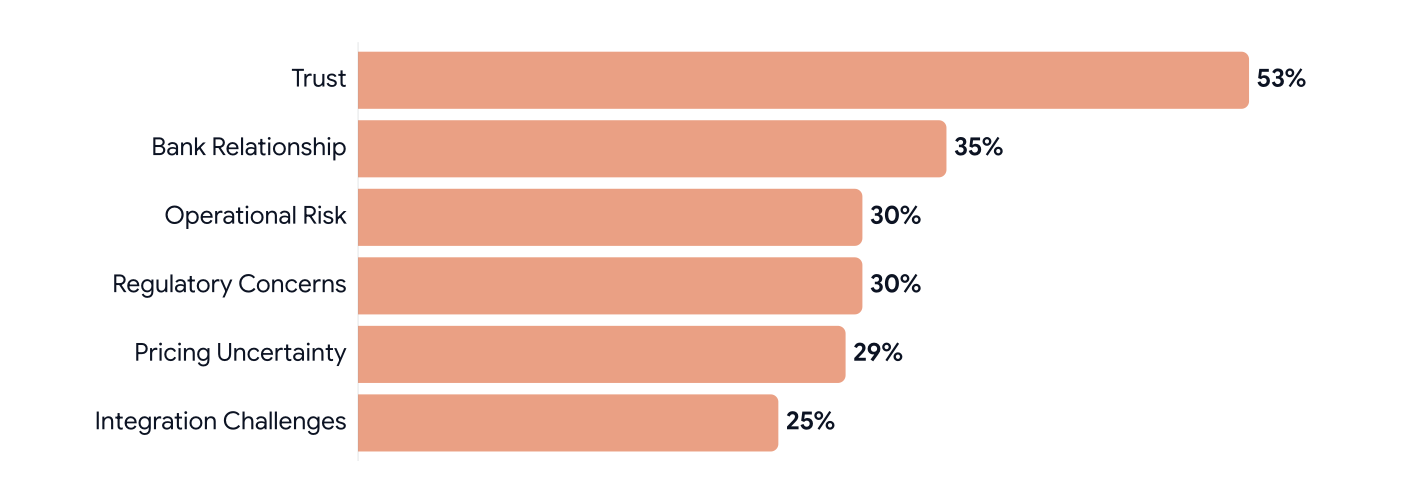

53% of ARP Digital's 2026 survey respondents cite trust as the primary barrier to switching payment providers. This finding requires careful interpretation. In qualitative interviews, it became clear that many respondents had never been approached by a credible non-bank alternative. For this segment, low awareness — not active satisfaction with their current bank — keeps them in place. Several interviewees specifically expressed concern that using a non-bank provider might trigger scrutiny from their own bank.

The barrier is institutional and informational, not technical. 63% of respondents indicate openness to digital payment platforms. The market is not resistant to change. It is waiting for a provider with the regulatory credentials to make change feel safe.

What Do Cross-Border Payments Actually Cost a GCC SME?

The true cost of a GCC cross-border payment is not the number on a transaction receipt. It is the cumulative total of five distinct cost layers, several of which are structurally designed to be invisible to the business paying them.

The anatomy of a GCC-to-Asia payment cost:

)

Sources: Airwallex, 2026; Razorpay, 2026; ARP Digital SME Survey, 2026

The FX markup is the primary mechanism of cost extraction in the cross-border payments industry, and it is deliberately designed to be invisible. Financial institutions and payment service providers apply a spread over the mid-market interbank exchange rate and embed it within the exchange rate offered to the client rather than displaying it as a separate line item. The Financial Stability Board (FSB) and G20 have established a roadmap targeting cross-border payment costs below 1% by 2027. Practical reality currently sits far above that threshold.

What ARP Digital's 2026 survey found on cost:

- 34% of respondents pay under 0.5% per transfer

- 27% pay 0.5–1% per transfer

- 23% pay over 1% per transfer

- 16% do not know what they pay

The 16% who cannot quantify their costs are not financially unsophisticated. They are the direct product of a cost architecture that embeds charges within exchange rates rather than disclosing them on a line-item basis. For an SME operating with net profit margins of 5%–10%, a cumulative 3%–5% loss in currency conversion and transaction fees can be the difference between a profitable trade and an unprofitable one.

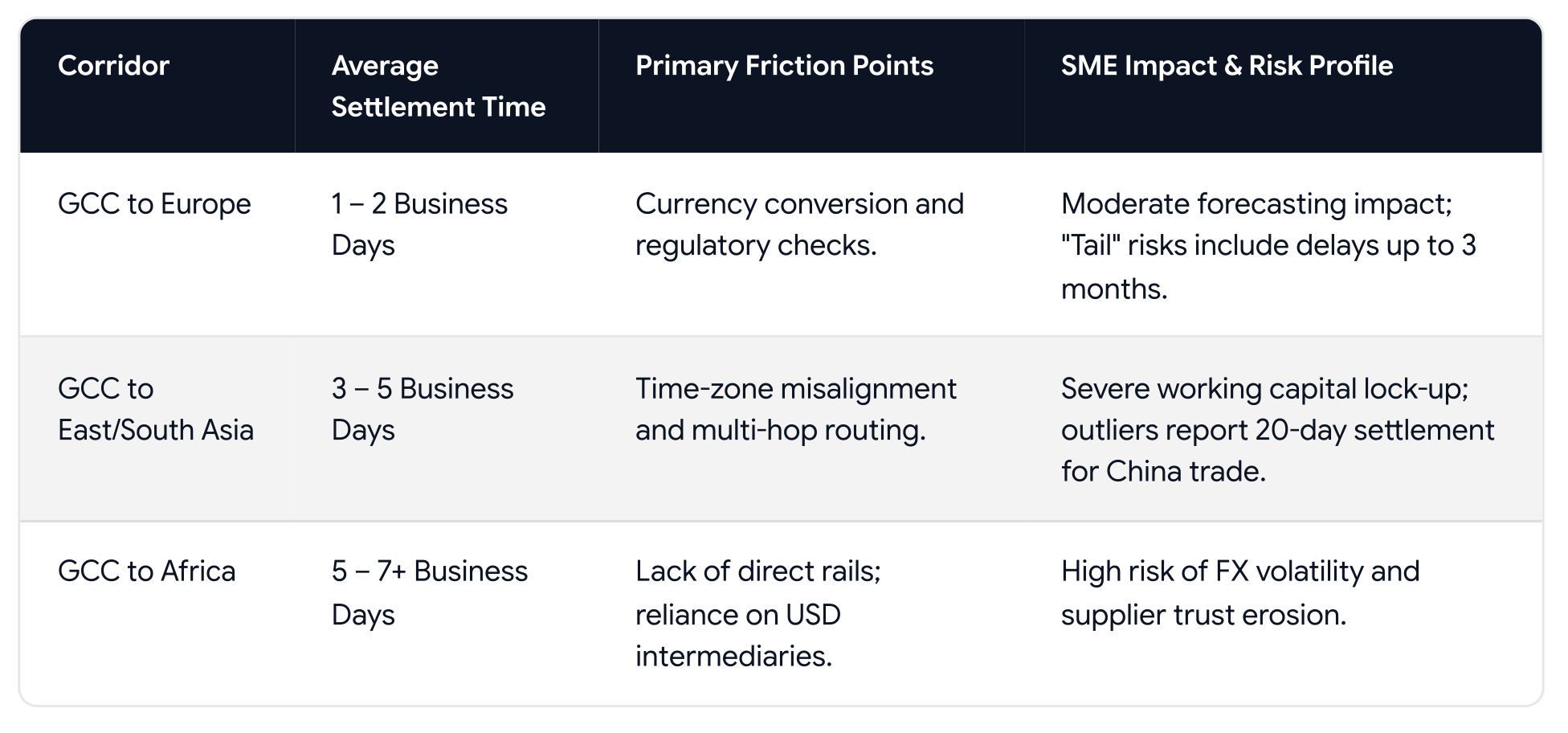

How Long Do GCC SME Payments Actually Take to Settle?

Settlement delays are the defining operational pain for GCC SMEs making cross-border payments. 47% of respondents in ARP Digital's 2026 survey cite delays as their primary problem — the single most frequently cited issue, ahead of poor FX rates (25%), failed or returned payments (24%), and unexpected fees (22%).

Settlement time distribution across all corridors (ARP Digital SME Survey, 2026):

These averages mask significant corridor-level variation:

The 3–5 day figure for GCC-to-Asia understates the reality encountered in qualitative interviews. One electronics importer in the survey sample reported an average of 20 days to clear payments to a Chinese supplier, a figure that reflects multiple intermediary hops, AML manual reviews, and reference code errors cascading across a chain with no visibility and no proactive notification.

Settlement delays are not merely inconvenient. They directly constrain working capital. SMEs plan inventory purchasing, payroll, and supplier commitments around expected settlement timing. When a single missing reference code or AML review shifts settlement by 48 hours, the disruption can cascade across an entire operational cycle. The practical result: businesses hold artificially high cash buffers, reducing their capacity to invest, hire, or expand.

What Business Damage Results from Payment Friction?

Payment friction creates downstream operational damage that does not appear in transaction cost comparisons but that is concrete and measurable at the SME scale.

Business impact reported by ARP Digital 2026 survey respondents:

Only 28% of respondents have ERP-integrated payment reconciliation. The remaining 72% reconcile manually, absorbing staff time and introducing error risk every payment cycle. This overhead is invisible in headline cost comparisons between banks and alternatives, but it is real and material at the SME scale.

The compounding nature of these failures is important. An SME that waits 3–5 days for settlement is simultaneously absorbing FX volatility during the settlement window, manually reconciling a payment that arrived short due to mid-route deductions, and managing a supplier relationship strained by unpredictable timing. The failures are not sequential, they are concurrent.

When a payment to a Chinese supplier stalls for 20 days, the production impact arrives not on the transaction statement but in missed deliveries and damaged supplier trust months later.

Which Payment Corridors Are the Most Painful for GCC Businesses?

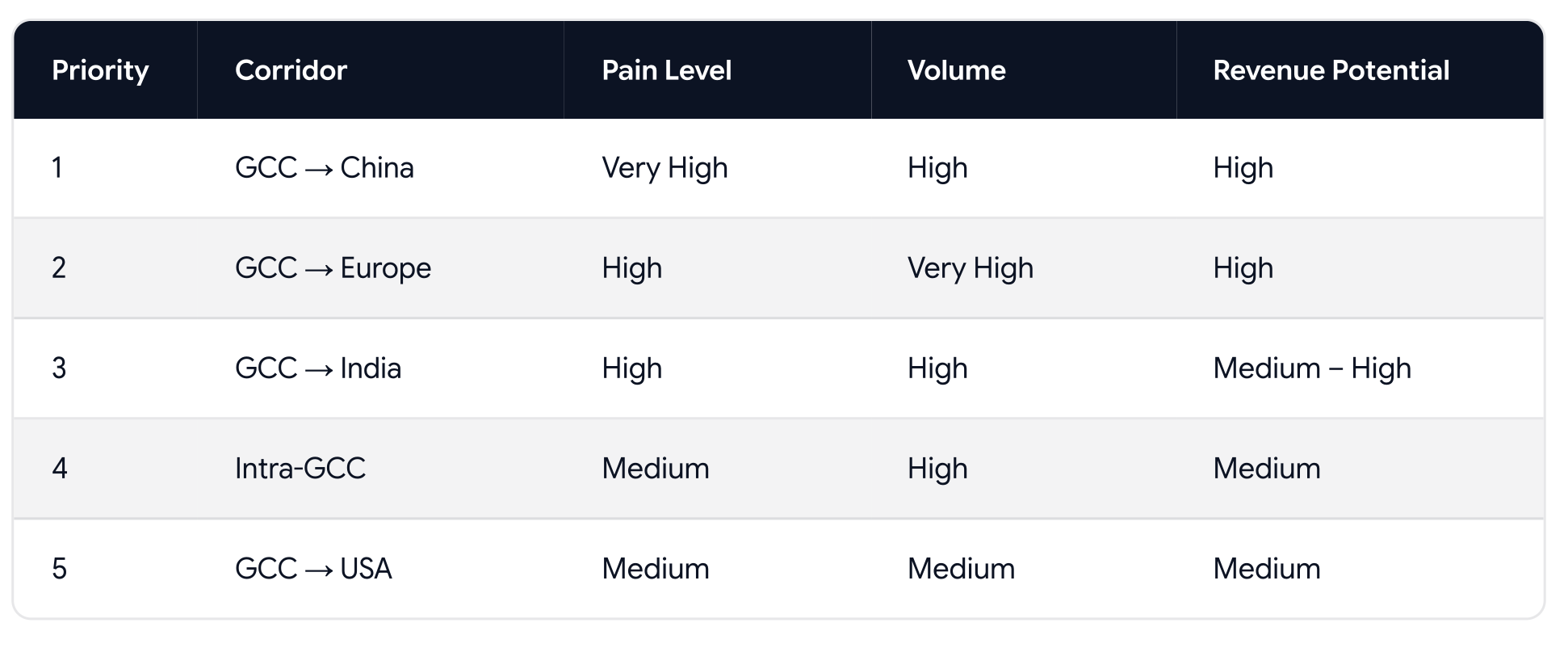

Not all corridors present equal pain or equal commercial opportunity. ARP Digital's 2026 research supports a clear priority framework based on the intersection of pain level, transaction volume, and switching intent.

The GCC-to-China corridor presents the highest concentration of pain alongside high transaction volumes, driven by the trading and wholesale importers who form 24% of the survey sample. These businesses operate with thin margins, predictable monthly payment cycles, and the highest concentration of supplier relationships in Asia, making payment efficiency a strategic concern, not merely an operational one.

GCC-to-Europe carries the highest absolute volumes (33% of all payment mentions) and broad industry relevance, making it the second-highest priority. The GCC-to-India corridor is positioned for rapid growth as the UPI-Aani payment bridge between Bahrain and India matures and as CEPA agreements reduce other bilateral trade friction.

Who Are the Highest-Value SME Buyer Segments?

Four distinct buyer personas emerge from the research data.

Trading Importer. Wholesale and manufacturing firms, 1–50 employees, revenue under USD 5 million. Pays China and Europe on a monthly-to-weekly cycle. Transaction sizes of USD 20,000–250,000. Primary pain: 3–5 day settlement and hidden FX costs. This is the highest-priority acquisition segment for any regulated alternative, highest trial willingness, clearest pain, most predictable payment cycles.

Regional Distributor. Construction and industrial firms, 10–50 employees, revenue USD 5–20 million. Pays GCC and Asian suppliers weekly. Primary pain: funds trapped in intermediary banks with zero tracking visibility, and compliance friction on larger transactions. Requires parallel testing before full commitment.

Services Exporter. Technology and professional services firms, 5–50 employees. Pays software vendors, marketing agencies, and contractors across multiple currencies. Primary pain: poor multi-currency FX rates and manual reconciliation overhead. High digital readiness; receptive to platform-based solutions.

Micro-Enterprise. 1–10 employees, revenue under USD 1 million, occasional small-value payments. Primary pain: flat fees that are disproportionate to transaction size. Lower near-term commercial priority, acquisition cost relative to payment volume makes this segment less attractive as a primary focus for regulated alternatives.

Would GCC SMEs Switch to a Non-Bank Payment Provider?

67% of ARP Digital's 2026 survey respondents indicate they would switch to a regulated, competitive alternative to their current bank. The composition of that intent matters as much as the headline figure.

Switching intent breakdown:

The 46% who would switch after a risk-free first transaction represent the most commercially significant finding in the research. A trial-first acquisition model, a single transaction through a regulated platform that allows a business to evaluate the experience before committing volume, is the single most effective conversion mechanism available in this market.

What barriers are preventing the switch?

Trust, as the primary barrier, must be understood in its market context. In qualitative interviews, the majority of respondents citing trust as a concern had never been approached by a credible, regulated non-bank alternative. The trust deficit is not about prior bad experience with fintech, it is about the absence of verifiable regulatory credentials in the alternatives they have encountered.

What Does a Competitive Alternative to Bank Settlement Need to Deliver?

The cross-border payment problem for GCC SMEs is not a technology problem. The technology to deliver same-day settlement, transparent FX pricing, and real-time payment tracking exists today. It is a market structure problem, a legacy system optimised for institutional scale that has never been redesigned for the businesses that now drive the most significant trade growth in the region.

The research data makes the requirements for a competitive alternative unambiguous:

Transparent FX pricing at initiation. The exchange rate must be disclosed before the transaction is confirmed, not embedded in a post-settlement statement. 25% of respondents cite poor FX rates as a primary pain point, but the opacity of how those rates are constructed is equally damaging.

Same-day settlement on priority corridors. GCC-to-China and GCC-to-Europe are the benchmarks. Same-day settlement on these corridors resolves the primary operational pain for the highest-value SME segment.

Real-time payment tracking. Visibility from initiation to confirmation, accessible to the business without requiring a call to a relationship manager. The absence of tracking is not merely inconvenient, it exposes businesses to downstream supplier relationship damage they cannot anticipate or manage.

Compliance support as a standard service. 67% of surveyed SMEs employ ten or fewer people. They do not have in-house compliance teams. Regulatory guidance - on documentation requirements, corridor-specific rules, AML obligations - is a differentiator in this market, not an add-on.

A trial-first onboarding model. 46% of switching-intent respondents need a risk-free first transaction before committing payment volume. Providers that require full onboarding commitment before a first transaction experience will lose this segment to those that do not.

Frequently Asked Questions

What are the most common cross-border payment problems for GCC businesses in 2026?

Settlement delays are the most frequently reported problem, cited by 47% of GCC SMEs surveyed by ARP Digital in February 2026. Poor FX rates follow at 25%, failed or returned payments at 24%, and unexpected fees at 22%. The combination of these issues — slow settlement, opaque costs, and mid-route deductions — creates compounding operational and financial damage for businesses making regular international payments.

How long does it take to transfer money from the GCC to China?

GCC-to-China payments typically take 3–5 business days to settle through conventional banking channels, according to ARP Digital's 2026 SME survey. However, qualitative research identified an electronics importer averaging 20 days for payments to Chinese suppliers — a figure reflecting multi-hop correspondent routing, AML manual reviews, and reference code errors in a chain with no tracking visibility.

How much does a cross-border payment cost for a GCC SME?

The total cost of a GCC cross-border B2B payment includes origination fees (0.5%–1.5%), SWIFT network fees (USD 10–50 per transfer), intermediary lifting fees deducted mid-route, an FX markup of 0.5%–3.0% above interbank rates, and jurisdiction-specific compliance costs. The cumulative total typically ranges from 1% to 5%+ of transaction value. In ARP Digital's 2026 survey, 16% of GCC SMEs could not quantify what they paid per transfer — a direct result of costs embedded in exchange rates rather than disclosed as line items.

What is correspondent bank de-risking, and how does it affect GCC payments?

Correspondent bank de-risking refers to the withdrawal by global tier-one banks from correspondent banking relationships in markets they consider high-compliance-cost, including MENA. When a GCC bank loses a direct correspondent link to a foreign clearing hub, it routes payments through replacement intermediaries — adding cost, settlement time, and opacity at every additional hop. The FATF has noted that de-risking, by pushing legitimate flows into less transparent channels, runs counter to the risk-based approach it was designed to promote.

Would GCC SMEs switch from their bank to a fintech payment platform?

67% of GCC SMEs surveyed by ARP Digital in February 2026 indicated they would switch to a regulated, competitive alternative. Of those, 46% said they would switch after a single risk-free first transaction. The primary barrier to switching is trust, cited by 53% of respondents — a function of low awareness of credible regulated alternatives rather than active satisfaction with existing banking providers.

What payment corridors have the highest pain for GCC businesses?

The GCC-to-China corridor presents the highest concentration of pain, driven by 3–5 day (and in some cases 20-day) settlement times and multi-hop correspondent routing. GCC-to-Europe carries the highest absolute payment volumes but lower average settlement delays. GCC-to-India is the third priority, growing rapidly as CEPA agreements and digital payment bridge infrastructure improve corridor efficiency.

Methodology

Based on structured surveys and depth interviews with 200+ GCC and MENA SME respondents, conducted by ARP Digital in February 2026. Sample is predominantly Bahrain-headquartered (78%), with UAE, Saudi Arabia, and other MENA markets represented.